Planning & Analysis

Process Solutions

Companies can no longer afford losses from ineffective trade promotions.

CPG companies often miss deduction errors in trade promotion management. These are small mistakes that quietly drain millions from their bottom line. Retailer chargebacks can build up unnoticed, until they surface at the worst possible moment. Imagine facing an audit or a board meeting, suddenly having to justify millions in unexplained write-offs.

“From what I’ve seen, it’s just like a health issue. At first, people ignore it, pushing it under the rug. The deductions pile up, they start aging, and no one reacts. Then, one day, like any other health problem, it hits hard.

Suddenly, management starts asking tough questions, and the scramble begins. Unfortunately, by that time, it’s already too late. The deductions have piled up, and clearing them in a meaningful way becomes incredibly difficult.“

— Haroon Jafree, CEO of EA

Learn how trade promotion deductions can drain millions from your profits. This guide will help you:

This article highlights the (often large and hidden) costs companies absorb from ineffective trade promotion management. It also outlines how to avoid them.

Trade promotions are meant to drive volume, revenue, and market share. But more sales do not automatically mean more profit. For instance, when TPM is ineffective, trade spend can grow faster than revenue. Promotions look successful on the surface, while margins erode underneath. The result is a gap between what leadership thinks was spent and what the business actually absorbed.

These losses rarely show up as a single line item. They surface as:

The root causes are mostly similar. Weak planning, inaccurate accruals, or poor coordination between teams.

Two areas determine whether trade promotion management succeeds or fails:

Planning is owned by the sales team. It starts with building realistic estimates for:

Accruals are calculated by the accounting/finance team, but they are only as good as the data coming from the plan/budget.

Based on the sales team’s planner, accounting records trade spend accruals. These accruals must be reviewed and updated consistently throughout the promotion period.

Here’s a simplified sales team’s budget/planner:

| Budget | |

| Selling price | $4 |

| Promo Rate/ Discount | 0.75 |

| Quantity | 10,000 |

| Expected Revenue | $40,000 |

| Trade Spend | $7,500 |

| Trade Spend % | 18.75% |

Budgeted trade spend is calculated as: Quantity*Rate

10,000*0.75=$7,500

In the above example, a promotion may be planned with $7,500 in trade spend. But the actual spend may end up closer to $11,000, as can be seen below:

| Budget | Actual | |

| Selling price | $4/unit | $4/unit |

| Promo Rate/ Discount | 0.75 | 0.75 |

| Quantity | 10,000 | 14,000 |

| Expected Revenue | $40,000 | $56,000 |

| Trade Spend | $7,500 | $10,500 |

| Trade Spend %* | 18.75% | 18.75% |

*Trade Spend %= Trade Spend/Revenue

In actual, 4000 more units were sold than planned. If accruals are not updated on-time for $3000 (10,500 – 7500), then that difference goes unnoticed until it’s too late.

Worse, if senior management approved only a $7,500 budget, any spend above that threshold should trigger additional approvals. Without timely updates, these controls fail.

This is where ineffective TPM becomes costly, because no one adjusted the numbers as reality changed. Adjusting accruals allows teams and senior management to see when promotions are deviating from plan and requiring additional accruals.

Example 2: In this example, we consider what happens when the budget includes promotional quantities and non-promotional ones:

| Budget | Actual | Variance | |

| Selling price | $4 | $4 | |

| Promo rate | 0.75 | 0.75 | |

| Non-promo quantities sold | 5000 | 2000 | (3000) |

| Promo quantities sold | 10,000 | 15,000 | 5000 |

| Revenue | $60,000 | $68,000 | $8000 |

| Trade Spend | $7500 | $11,250 | $3,750 |

| Trade Spend % | 12.50% | 16.54% | +4.04% |

In the above example, there are product quantities being sold with and without promotions. The example shows that the revenue is 13.33% more than the budget, but trade spend is higher by 50%. Trade spend increased disproportionately compared to revenue growth. This indicates that the promotion drove volume, but the margins decreased.

If TPM only tracks revenue or unit growth, this promotion would look like a win when, financially, it wasn’t.

Trade spends rose from 12.5% to 16.54% of revenue. That 4.04% increase means the company paid significantly more for each dollar of revenue. Even with higher sales, the promotion delivered lower quality revenue.

When promo and non-promo quantities are not estimated accurately, the resulting accruals are also flawed. Since accruals are calculated based on planned volumes, any weakness in volume forecasting (by the sales team) directly leads to mismanaged trade spend accruals.

As actual results come in, large deviations* between plan and actual require investigation. Finance teams need to understand what is driving the variance, not just that a variance exists.

In reality, the actual figures will likely deviate from the plan, but the teams should decide on the limit they can deviate from. If they differ from a material amount, then the finance team must ask sales teams questions such as:

Without clear answers from the sales team, finance cannot accurately adjust accruals or control trade spend. This is also one of the ways leading to ineffective trade promotion management.

Misaligned teams lead to costly trade promotion failures.

Haroon Jafree, CEO of EA, states, “One of the common themes I’ve seen, even with some big companies, is that nobody understands the whole picture. So they try to attack bits and pieces of it. But unless it is solved from start to finish, addressing all the different areas of this process and its cross-functional aspects together, you can never bring this process together in a meaningful way.”

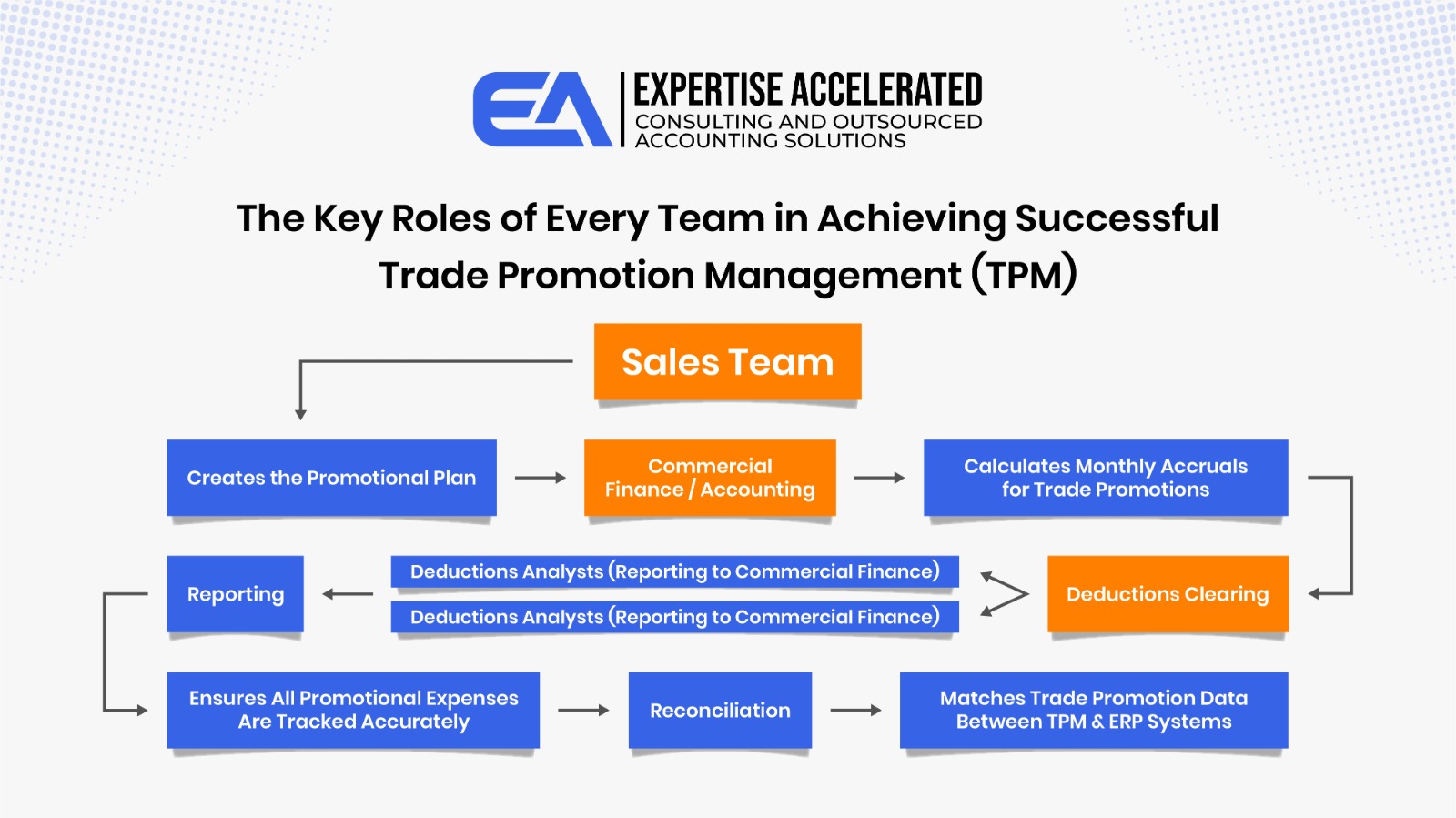

For trade promotions management to be a success, there has to be a strong collaboration between the cross-functional teams (i.e. sales, accounting, and deduction analysts teams). (This is shown in the image below). Many companies struggle to align these teams, leading to inefficiencies and revenue leakage.

*note: the individual teams are highlighted in the orange boxes.

Here’s how the process typically flows:

Since trade promotions involve multiple departments, a lack of collaboration can create major inefficiencies such as:

-Sales, finance, and accounting often work in silos, leading to misalignment in promotional spending.

-Deductions may go unverified or disputed too late, resulting in lost revenue.

-Without a clear reconciliation process, tracking trade promotion expenses becomes challenging.

Many companies also lack a culture of cross-functional collaboration, making it difficult to align teams and streamline operations. As a result, instead of driving revenue, trade promotions become disorganized, inefficient, and costly.

Individuals involved in trade promotions management often become frustrated because they attempt to fix issues within their own department. However, since this is a cross-functional process, improving just one part of it won’t resolve the entire problem unless all areas are streamlined and aligned. As a result, inefficiencies persist, and frustration grows.

To address this, management must first understand the entire trade promotions process. They should know how different functions interact and where breakdowns occur. From there, they can deploy the right solutions, such as specialized software, expert consultants, and accounting expertise, to ensure a cohesive, efficient system that works across all departments.

Trade promotions are one of the largest and least understood investments CPG companies make. Without structure and accountability, it’s difficult to know which promotions drive incremental growth and which contribute to eroding margins.

Here’s a simplified example of a PNL for a $10 million U.S. CPG company:

Income Statement

For the Year Ended December 31

| Amount (USD) | |

| Net Revenue | 10,000,000 |

| Cost of Goods Sold | 5,500,000 |

| Gross Profit | 4,500,000 |

| Operating Expenses: | |

| Trade Promotion Spend | 2,000,000 |

| Salaries & Wages | 900,000 |

| Marketing (Non-Trade) | 400,000 |

| General & Administrative | 350,000 |

| Distribution & Freight | 300,000 |

| Other Operating Expenses | 150,000 |

| Total Operating Exp. | 4,100,000 |

| Operating Income | 400,000 |

| Interest & Taxes | 150,000 |

| Net Income | 250,000 |

What This Shows

In this scenario, even a 5–10% inefficiency in trade spend could wipe out most of the company’s profit.

A CFO who has accurate and organized trade promotion data has visibility into whether promotions are actually driving margin, not just revenue. He can confidently tell financiers the process is controlled, reconciled, and best-in-class (just how they want). There is no fear of large reconciliation gaps between systems, because syncing is disciplined and consistent.

When trade promotions are organized, accruals are reasonable estimates, and deductions are validated. You know what’s real. You know what’s recoverable. You know which promotions worked and which ones burned margin.

As a CFO, you don’t squint at spreadsheets trying to reconcile three different versions of the truth. You don’t sit in meetings where sales say one number, finance says another, and deductions tell you something else entirely.

The numbers make sense.

Claims come in. Invalid deductions are flagged. Disputes are handled. Accruals are adjusted. ROI is measured. The story of the trade spend is visible.

Now compare that to fragmented data. Siloed teams. Promotions launched without disciplined tracking. Deductions piling up in aging buckets. Accruals that are very different from reality. When this happens, none of the dashboards that one might be looking at will “talk” to each other. There will be composite reports built on incomplete inputs.

You might be told that trade spend is 20% of revenue, but you can’t confidently say what the return was.

Forecasts are built on numbers you don’t fully trust. Cash flow surprises you. Sales blames execution. Finance blames the process. Deductions quietly erode margins.

And over time, something starts to stress. Because a CFO isn’t meant to operate in fog. A CFO needs a line of sight. Needs alignment. Needs reasonable accruals and disciplined deduction management to make trade promotions a success.

Ineffective TPM is rarely caused by one big failure. It usually comes from small breakdowns across planning and execution. The good news is that most of these issues are preventable with the right processes in place.

Sales teams must develop reasonable estimates for promo and non-promo volumes, expected revenue, and trade spend.

Overly optimistic assumptions distort accruals from day one and make it difficult to measure the actual promotion performance.

Plans should reflect historical behavior, customer-specific patterns, and expected cannibalization, not just growth targets.

Accruals should not remain static once a promotion is launched. As actual sales and spend data come in, accruals must be reviewed and adjusted regularly.

Periodic updates:

Waiting until the month-end or quarter-end is too late. Teams should review promotion performance while it is live, at both promotion and period levels.

Early visibility allows teams to correct course when:

Sales, finance, accounting, and deductions teams must operate as one system, not in silos. Regular reviews of planners, accruals, and results ensure everyone is working from the same numbers.

The deductions team plays a critical role in effective TPM. They must be able to validate deductions thoroughly and consistently.

Without a proper validation process, invalid or duplicate deductions can go unnoticed. When required documentation is skipped, claims are not disputed on time, causing the company to lose money unnecessarily.

Strong deduction controls ensure that only legitimate trade spend is recognized and that recoverable dollars are not written off due to process gaps.

Without periodic planner and accrual updates, trade promotion management becomes costly. With effective TPM:

must trigger a review during the promotion, not after.

Variance analysis should not be a reporting exercise. Finance teams must understand what is driving deviations and why.

When large gaps appear, teams should quickly identify:

This closes the loop between planning and execution.

Retailer chargebacks are one of the sources of revenue loss in trade promotion management. They accumulate gradually, often going unnoticed until they surface as significant write-offs during audits or period-end reviews.

Many companies only review a fraction of incoming deductions. The rest are either written off without investigation or left to age in backlog buckets until recovery becomes impractical.

A stronger approach is to verify a significantly higher percentage of chargebacks than most internal teams can manage on their own. Rather than limiting review to only the largest claims, a tiered verification process ensures high-value deductions receive full scrutiny, while smaller ones are systematically batched and reviewed for patterns. This way, nothing is written off by default, and recoverable dollars are not lost simply due to capacity constraints.

When businesses establish a consistent and thorough validation process, the impact goes beyond recovering individual claims. Retailers begin to recognize that every deduction will be scrutinized. Over time, this reduces the volume of unjustified claims, improves cash flow, and creates a healthier dynamic with retail partners.

The key is building a system that is both rigorous and sustainable. For many companies, this means leveraging cost-effective, specialized resources to conduct verification at scale, without overburdening internal finance or deductions teams.

When deduction verification becomes a disciplined, ongoing process, it shifts from damage control to financial control. Companies stop absorbing losses they were never obligated to take, and they gain clearer visibility into which deductions are legitimate, which are recoverable, and which patterns require upstream correction in the promotion plan itself.

Trade Promotion Management (TPM) in the CPG industry refers to the process of planning, executing, tracking, and settling promotional activities with retailers, all while maintaining financial accuracy and operational efficiency.

From a finance and operations perspective, TPM plays a critical role in:

Effective TPM allows CPG companies to optimize their promotional investments, accurately plan and categorize liabilities, strengthen retailer relationships, and enhance brand visibility in the marketplace. Without a robust TPM strategy, businesses risk failing to deliver profitable results or meet key performance indicators (KPIs).

Many CPG companies lack processes for best practices. This can lead to issues such as not clearing deduction claims on a timely basis.

Some prevalent challenges include relying on manual calculations, which can lead to inaccuracies; lack of integration both internally and with external partners; and the inability to plan promotions based on analytics.

Here are the key challenges faced by CPG companies in managing Trade Promotion Management (TPM):

Technology can improve Trade Promotion Management (TPM), but only if it’s used the right way.

Many CPG companies think that just installing TPM software will fix their problems. But software alone isn’t enough. If the management team doesn’t understand the full promotion process, from planning to deductions, the software won’t help much.

To get real value from technology, companies need to:

In short, technology helps. But only when there’s strong teamwork, clear processes, and support from the top. Otherwise, it’s like buying a plane without learning how to fly it.

To achieve effective Trade Promotion Management (TPM), there are several best practices that CPG companies should follow.

First, strong management sponsorship and understanding is essential. Leadership needs to fully understand the entire TPM process, from start to finish. Without this top-down support and vision, it’s difficult for the company to align all departments and drive successful outcomes.

Next, cross-functional team alignment is key. TPM is a cross-functional process, so it’s crucial that all teams, including sales, finance, and accounting, are on the same page. The individuals involved in TPM should understand the entire process, not just their specific tasks, and work together toward a common goal.

Additionally, companies need to ensure proper staffing across different functional areas. These individuals should have the expertise needed for their specific roles but also a holistic understanding of how their work fits into the larger process. This ensures that everyone is contributing effectively to the TPM effort.

Training and commitment are also critical. A successful TPM strategy requires commitment from everyone involved. This includes investing in training to ensure that all team members know how to use the TPM tools effectively and understand the importance of their roles within the broader vision.

Finally, companies must make effective use of technology. Implementing and properly utilizing TPM software tools helps streamline the process. The software should be designed to generate the necessary critical reports that provide the management team with accurate, actionable data to drive decisions.

Effective TPM requires clear vision, cross-functional collaboration, proper staffing, continuous training, and the strategic use of technology. These practices ensure everyone is working toward a common goal and that the process runs smoothly from beginning to end.