Planning & Analysis

Process Solutions

Generally Accepted Accounting Principles (GAAP) are the standard rules used in the U.S. for creating clear, accurate financial reports. They help businesses present finances consistently for trust and comparison.

GAAP principles organize accounting and clarify financial information. In this guide, we’ll break down what GAAP is, who uses it, and why it’s essential.

Generally Accepted Accounting Principles are financial reporting standards set by the FASB and GASB. The FASB established GAAP after the 1929 crash to prevent misleading reports and update it.

These principles ensure accurate and transparent financial information. U.S. traded companies, nonprofits, and government organizations must follow GAAP. Other businesses may also choose to adopt these principles. GAAP guides companies in reporting revenue and classifying assets, aiding investor comparisons.

An example of GAAP is when an accountant reports revenue when earned, even if cash isn’t received. The accountant records expenses at the time of sale, not when the company pays cash.

The most important GAAP principle is likely the objectivity principle. This principle mandates that all financial statements must rely on objective evidence. This ensures accuracy and transparency while avoiding personal bias. Consistency means using the same rules in every report, making it easy to compare. Honesty ensures clear and fair reporting, building trust. Accuracy ensures that financial reports are reliable and show the true state of the business. Finally, the future outlook assumes the business will keep running, which helps assess its financial health.

Common GAAP violations include using accelerated depreciation methods allowed by the tax code. Other violations involve having varying rent payments and capitalizing overhead costs. This includes misapplying overhead costs to inventory valuation.

GAAP requires four financial statements: balance sheets, equity statements, cash flow statements, and income statements. It also requires income statements. These show a company’s financial health and growth possibility.

U.S. publicly traded companies must follow GAAP. This comprises government entities, profit, and non-profit organizations. Private businesses can choose to follow GAAP for consistency but aren’t required to.

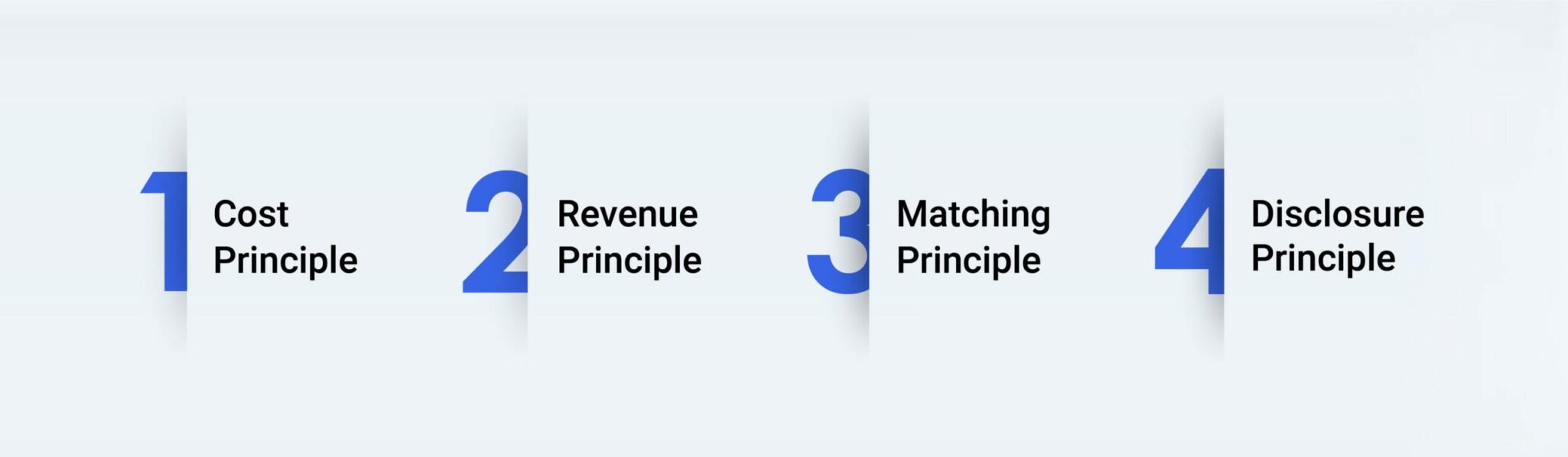

The Cost Principle says that a firm should record assets at their actual sale price, not their recent market value. For example, if a firm buys equipment, it will list the price paid for that equipment in its financial statements, even if its value has risen. This approach keeps financial records consistent and reliable.

The Revenue Recognition Principle states A firm records revenue when earned, even if cash isn’t received. For instance, A company records income in March for services provided, even if payment arrives in April. This approach represents the company’s earnings over time.

The Matching Principle requires reporting expenses in the same period as the income. For example, If you incur costs to produce products in a month, record those expenses with that month’s sales. This stops companies from inflating profits, giving a clearer view of true earnings.

The Full Disclosure Principle demands that companies provide all relevant financial details. This means providing everything necessary to understand the company’s financial situation. Additionally, it possesses details about threats or possible issues. Being transparent helps people make better decisions based on the financial statements.

Public traded companies must follow GAAP, as required by the Securities and Exchange Commission (SEC). External auditors check for GAAP compliance. While not required, many private companies use GAAP since lenders often prefer it for financial agreements.

GAAP makes it easier to trust and understand a company’s financial information. Without GAAP, comparing financial reports even from similar companies becomes difficult.

According to Bloomberg, The SEC is considering replacing U.S. accounting rules with simpler international ones. This could help create a single global standard, making it easier to trade worldwide. But, this new approach has its risks.

Ten years ago, it would have been difficult to think about getting rid of GAAP. At the time, investors and firms viewed GAAP as the best way to report earnings and financial details. As European and Asian companies adopted local methods, GAAP seemed to stay preferred. Accountants everywhere favored GAAP for its consistency and clarity.

According to HBR, Many companies now share a number called non-GAAP earnings along with their regular GAAP earnings. Non-GAAP earnings leave out some costs that don’t involve cash or aren’t important for understanding how the company will do in the future.

First, they show their GAAP earnings and then explain any changes made to get to the non-GAAP number. Companies invest in things like research, branding, customer relationships, software, and skilled workers. Companies count these investments as expenses, which can lower reported profits. If a company spends more to grow in the future, it might seem like they’re losing money. To fix this, many companies show a non-GAAP number that adds back these costs.

GAAP is rules-based, meaning it has strict guidelines, while IFRS is principles-based, allowing for more flexibility.

GAAP | IFRS | |

| Conceptual Framework | Not official; rarely used | Official guidance is provided |

| Preparing Financial Statements | Needs specific details for possible liquidation | No specific rules for this |

| Forms of Financial Statements | Encourages comparative data and requires consolidation for subsidiaries. | Requires comparative data for key disclosures; some subsidiaries may consolidate. |

| Statement of Financial Position | Follows strict SEC rules for line items | Requires key line items but allows flexibility |

GAAP keeps financial reporting fair, clear, and easy to understand. It is vital for making informed decisions about investments and business finances. Following GAAP helps companies produce trustworthy financial statements that build trust.

To improve your accounting practices, seek advice from experts on implementing these standards.