The previous quarter was very promising on paper.

Sales were strong. Revenue targets were met. The team hailed what appeared to be a triumphant season.

And yet a couple of weeks later, there was another reality.

Suppliers were waiting to receive payment. The payrolls were closing in. And the finance department was posing a vexing question: Where is the money?

The problem was not sales. The issue was time – the time it takes the revenue to get into the bank. The money may take weeks or even months to be transferred from accounts receivable to cash after issuing an invoice and receiving payment. This is where a very crucial yet somewhat neglected financial measure is brought in: DSO – Days Sales Outstanding, the figure of the duration, in which a company takes to get the money after the sale.

Understanding DSO and Its Calculation

Increased DSO is a warning sign. Slow collections, poor working capital, and liquidity pressure compel companies to borrow or postpone investments. Conversely, best performers tend to receive cash within 30 days or less, whereas slower companies may require 45 days or more holding on to capital at a cost which is much larger than it appears on paper.

For contemporary leaders in finance, DSO is not merely a figure on a dashboard but a performance metric. It affects your working capital, cash conversion cycle, and financial health.

Regardless of whether benchmarking across the industry or refining collection processes, it is imperative to have in-depth knowledge of DSO to diagnose cash flow problems before they turn into a crisis. CFOs who focus on planning, forecasting, and liquidity management use this measure to identify issues promptly and make data-driven decisions.

When your receivables are tied up inefficiently, the company may face issues, such as delays in paying vendors, strained relations with suppliers, and limited budget flexibility.

DSO to CFOs shows the efficiency of your receivables and the financial health of your business.

What is DSO, and How Is It Calculated?

Days Sales Outstanding (DSO) is calculated as the average number of days a business takes to receive payment after a sale. The standard formula is:

| DSO = (Total Credit Sales/Accounts Receivable)×Number of Days in Period |

To illustrate this, assuming that a company has a balance of $500,000 in accounts receivable and a rate of sales of credit amounting to 2,500,000, the DSO of that month will be:

| DSO=(2,500,000 x 500,000) × 30 =6 days |

Six days of capital caught up before it gets to your bank account. This is six days of capital that every CFO counts carefully, since every additional day of DSO costs your company in terms of opportunities to invest, interest on outstanding debt, or terms of payment.

DSO is closely related to measures such as accounts receivable turnover, invoice payment terms, and payment cycles. A high DSO is associated with slow receivables turnover and a long invoice payment cycle, and it may be reflected in a longer cash conversion cycle.

The industry benchmarks indicate the stakes. For instance:

- APQC (2025) study indicates that in a manufacturing company, the average DSO is 46 days, with the best taking only 30 days and releasing a lot of working capital.

- SOA in SaaS and subscription business models can be as short as 15-20 days due to automated invoicing and online payments – a distinct competitive edge in cases of capitalizing growth or developing a product.

Learning about DSO also entails understanding its impact on financial statements. High DSO dilutes cash on hand, inflates accounts receivable, and could indicate a potential liquidity risk to investors or lenders.

On the other hand, a low DSO improves working capital management and financial liquidity. It is an indicator of efficient operations, all of which are essential to CFOs’ efforts to maintain a healthy balance sheet.

In a nutshell, DSO is not only a diagnostic tool but also a strategic tool. With its tracking, the heads of the finance team can identify inefficiencies in invoice processing, flag credit risks, and compare performance against industry norms for a company operating in competitive markets.

Factors That Influence DSO

For CFOs, it is not half the battle to be aware that DSO exists, but to gain insight into what will increase or decrease DSO. Delays in payments are not just inconveniences; they indicate idle cash that could have been reinvested in the business to expand, enhance relationships with suppliers, or develop business strategies. Knowledge of the levers of DSO enables financial leaders to maximize cash flow, reduce risk, and enhance financial flexibility.

Customer Payment Behavior and Credit Policies

A customer payment behavior is usually the single biggest contributor to DSO. Do invoices get paid on time, or are they paid late, causing cash flow bottlenecks? CFOs are aware that a small number of slow-paying customers can cause an extreme change in DSO.

- Policies on credit: Offering easy terms without tracking a history of debt repayment increases the risk of DSO. A survey by the Credit Research Foundation in 2024 shows that, on average, companies that strictly evaluate their credit and have shorter payment terms have a DSO that is 20-25% lower than that of lax companies.

- Trends in payment: Customers who pay by check can take weeks, while automated ACH or digital payments reduce the time to receive payment by 40%.

The active use of credit and the active monitoring of payment trends can transform DSO from a passive parameter into a strategic tool for cash flow control.

Operational Processes

Customers not only affect DSO; internal processes are also vital. Slow invoicing, disjointed accounts receivable departments, and ineffective collection processes can unnecessarily prolong DSO.

- Invoice processing: Sluggish processing or invoice errors may add days, possibly weeks, to the collection process. Organisations with automated invoicing define that processing time has decreased by 30-50, which has a direct impact on DSO.

- Collection cycles: Frequent follow-ups and organized collection policies minimize the payment lag. Firms that have specially set up AR teams and escalation procedures have reduced and smoother DSOs.

- AP vs AR alignment: When CFOs align accounts payable and accounts receivable processes, they realize improved cash flow, fewer disputes, and a shorter DSO. For example, certain manufacturers align AR collections with AP disbursements to establish a self-balancing cash flow.

Industry Benchmarks and Cash Flow Optimization

Finally, context matters. DSO is subjective and depends on industries and business models. Knowledge about benchmarks assists CFOs in establishing attainable goals and outliers.

- Retail has a DSO of 40-50 days on average, whereas tech and SaaS businesses can aim at 15-25 days, as they have subscription-based and automated billing.

- Efficient companies relate DSO to overall cash flow and working-capital optimization plans. A reduction in DSO not only frees up cash but also improves liquidity ratios and the consolidated balance sheet, allowing companies to invest freely.

DSO is motivated by customer behavior, internal operational efficiency, and the industry setting. Mastery of these factors by CFOs enables them to control one of the most important performance levers in the financial arena: the speed of cash turnover.

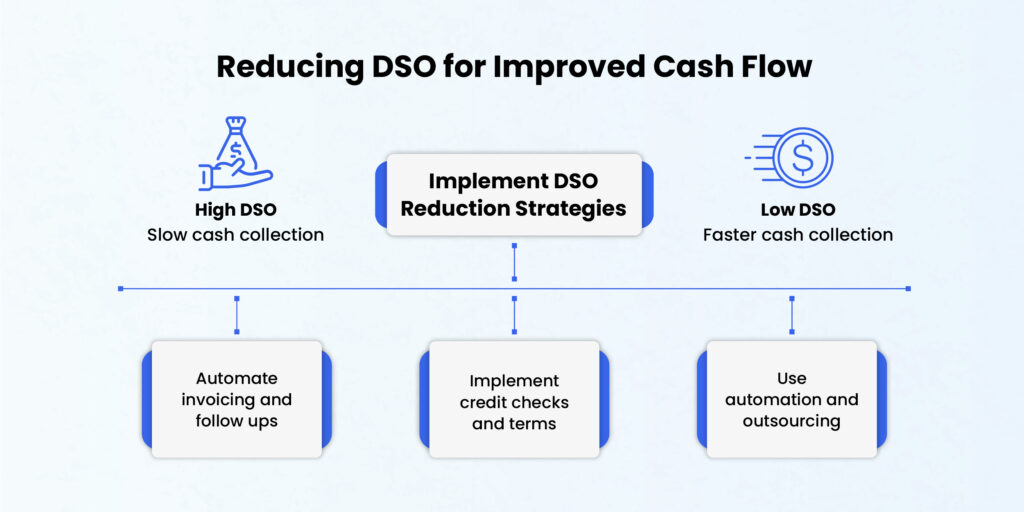

Strategies to Reduce DSO

For CFOs, it is not all about going after overdue invoices to reduce DSO, but rather about developing a rigorous, repeatable structure that accelerates cash inflows and enhances the company’s wellness.

Cash is lying around unspent every day; it is capital that cannot be used to grow, pay suppliers, or make strategic investments. With a focus on the underlying causes, finance leaders will be able to make DSO not a reactive measure but rather an active financial driver.

Streamline Receivables and Collection Processes

Effective receivables management forms the basis for reducing DSO. Optimizing collection processes by firms not only speeds up the cash inflows but also decreases administrative overhead and errors.

- Receivables optimization: Invoices will be generated and automatically delivered to ensure clients receive the correct bills within a prescribed timeframe. Studies conducted by the Credit Research Foundation indicate that DSO decreases by 20-30 percent in firms that use automated invoicing reports rather than manual operations.

- Collection effectiveness: Payment cycles are reduced through organized follow-ups, reminders, and escalation procedures. To illustrate, an invoice reminder system consisting of 3 steps, used by some B2B SaaS companies within the first 10 days after invoice issuance, increases on-time payment rates by up to 25 percent.

- Productivity in invoice processing: The standardization of invoice systems in each department and their integration with AR systems will eliminate bottlenecks and errors and allow CFOs to maintain predictable cash flow.

Improve Credit Management and Payment Terms

Strategic persuasion of DSO can be achieved through proactive risk management and the formulation of clear credit policies by CFOs.

- Credit check: Review customers’ payment records and risk profiles before extending terms. Companies that segment clients by creditworthiness can set credit limits and terms that reduce the likelihood of the company owing money.

- Payment collection tactics: offer an incentive to pay on time (a 2 percent discount on the payment) within 10 days, or impose a penalty for late payment. Surveys of the industry have revealed that, with the assistance of early-paying discount programs on all its debt, it is possible to reduce the DSO by 3-7 days on average.

- Management of terms of payment: By matching your normal terms with industry norms, take operational realities into account. CFOs who do quarterly reviews and change terms retain closer control over receivables without creating tension with clients.

Leverage Technology and Outsourcing Solutions

The use of technology and strategic outsourcing is becoming an increasingly popular way to reduce DSO, as it makes AR operations more scalable and efficient for modern finance teams.

- Automation platforms, Digital AR platforms monitor invoice status, automate notifications, and create real-time dashboards for collections teams. Companies using AR automation report that payment cycles are 30-40 times shorter.

- AR operations outsourcing: Strategic invoicing and collections. Companies can outsource AR operations by engaging specialized providers, as outlined in our Outsourcing AP and Outsourcing AR blogs.

- Co-ordinated AP/AR policies: CFOs handling payables and receivables achieve a better predictability of cash flows and a better working capital; DSO is lower, and liquidity is also smoother across the company.

Result: Companies implementing such strategies can achieve observable transformations, including greater cash inflows, faster working capital cycles, and improved financial health. For CFOs, reducing DSO may not be a matter of efficiency but of opening up cash to grow, improving relationships with suppliers, and securing a stable financial position.

Conclusion: Turning DSO into a Strategic Advantage

Days Sales Outstanding (DSO) is more than just a number in a financial statement; it is a key indicator of cash flow efficiency and overall business performance. For CFOs and other finance leaders, DSO is an excellent tool that provides insight into a company’s ability to convert sales into ready cash, informing decisions about working capital, expansion, and financial stability.

DSO is affected in various ways by factors such as customer payment behavior, operations, and industry requirements. Ongoing monitoring and analysis enable finance departments to anticipate cash shortages, manage credit risk, and streamline financial processes before minor delays escalate into more substantial liquidity issues