Planning & Analysis

Process Solutions

A complete guide on the Double Declining Balance (DDB) Method to help you clearly understand value depreciation.

The Double Declining Balance (DDB) is a depreciation technique that identifies greater depreciation expense during the initial years of utilization of an asset and gradually decreases the expense during the subsequent month-end closings.

DDB does not equally distribute the cost as the straight-line method, but applies twice the straight-line rate of the remaining book value of the asset each year.

This forward-loaded framework is economically true to a large number of sectors. Value is not normally lost evenly on the assets. In the manufacturing industry, say a new piece of equipment will run optimally within the initial few years of being deployed to the manufacturing line. Gradually wear and maintenance will decrease the machine’s relative productivity. Technological changes may also lower the relative productivity of the equipment.

Hardware and specialized equipment used in technology-based industries may become obsolete even before they wear out.

Transport and logistics fleets tend to record the steepest drop in resale value during the first years of their operation because of the trend in mileage and market depreciation.

DDB will match accounting expense with the actual delivery of value of assets by accelerating depreciation. It acknowledges the fact that economic advantage is frequently primitive in time – advantage in production, or speed of processing, or a token of income-generating power.

DDB is normally implemented by companies whose asset performance and economic value decline at a high rate in the long run. In capital-intensive sectors like manufacturing, construction, and energy, the equipment will yield the highest output soon after purchase.

In the long term, efficiency could decline because of physical wear, maintenance pause, or, newer, more sophisticated options could be introduced in the market. This operational fact is reflected in the recognition of higher depreciation.

Increasing maintenance costs are also another determinant. Experience and research in the industry reveal that maintenance and repair costs tend to rise with the age of the asset. This is compensated by an accelerated depreciation, which apportions a higher amount of cost in the initial usage, and in effect, this is just a way of smoothing the total ownership cost throughout the life of the asset.

This gives a better reflective state of total asset economics to CFOs who are appraising capital expenditure decisions. Tax planning is also a convenient fact. Rapid depreciation lowers taxes paid on prior years, enhancing quick cash flow.

In the case of growing enterprises, particularly manufacturers, CPG brands that have reached scale in production, or a growth in the size of fleets by a logistics company, early tax savings may be returned into inventory, automation, research and development, or working capital. Although the timing of depreciation does not wipe off taxes, it moves the burden in such a manner that it can favour strategic reinvestment.

There is also the matching principle in accounting, which is reinforced by DDB. When an asset generates more revenue or efficiency benefits in its early years of operation, its recognition of higher depreciation expense in the early years of operation would cause more effective reporting of profitability. This is especially applicable in business where a competitive advantage is conveyed at the beginning of the industry by equipment or technology, which diminishes with time.

Adoption of DDB is, however, not entirely mechanical. It affects reported earnings, balance sheet asset values, financial ratios, and perception by investors. Before choosing a method, public firms and investor-supported firms often analyze the impact of accelerated depreciation on EBITDA patterns and capital efficiency ratios.

Finally, the Double Declining Balance approach is best suited where asset utilization trends, technology cycles, and economic value are declining to support a front-loaded cost system. It is not merely an accounting choice- it is a strategic financial choice that ought to be in accord with operational realities, along with long-term financial planning.

The Double Declining Balance depreciation formula is:

Depreciation Expense=Book Value at Beginning of Year×(2/Useful Life)

Where:

1÷5=20%

20%×2=40%

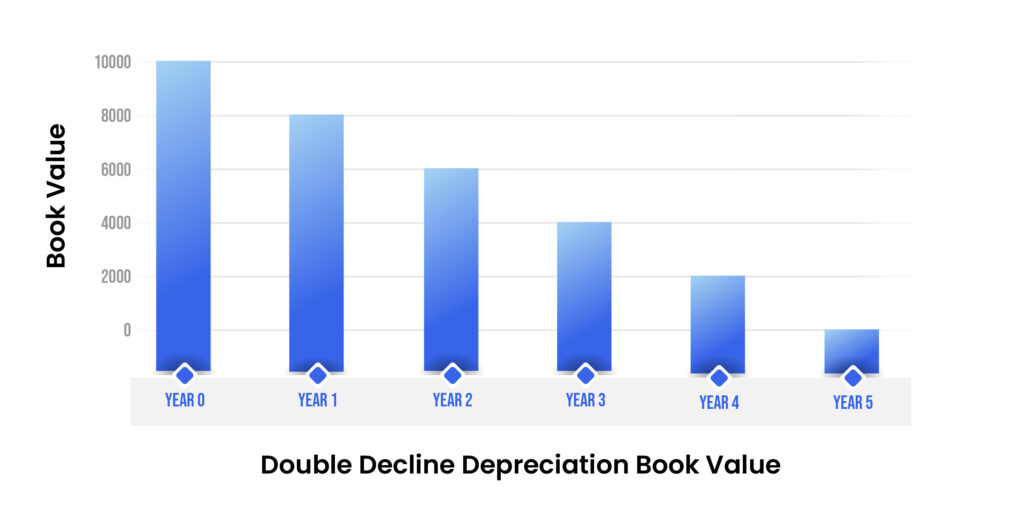

Year 1:

$10,000×40%=$4,000

Book value = $10,000 − $4,000 = $6,000

Year 2:

$6,000×40%=$2,400

Book value = $6,000 − $2,400 = $3,600

Year 3:

$3,600×40%=$1,440

Book value = $3,600 − $1,440 = $2,160

Year 4:

$2,160×40%=$864

Book value = $2,160 − $864 = $1,296

Year 5:

Adjust depreciation to reach salvage value:

$1,296−$1,000=$296

The DDB approach expedites the depreciation process, acknowledging increased cost during the initial years of the existence of the asset when it has the greatest contribution to the operations.

The amount of depreciation per year is computed on the basis of the beginning book value and not the original cost. This makes it possible to reduce the cost in the long run.

The depreciation should not ever depreciate the asset to a lower valuation than its salvage value. This limit has been respected in the last year by adjusting the depreciation.

In the manufacturing sector, machinery can be used to achieve optimum output in the initial years. The use of DDB allows the financial statements to report more expenses in case of high productivity of the asset. In the same way, in technology and transportation, the rapid obsolescence or resale depreciation is well captured.

In the first years of asset utilization, early higher depreciation is offered with tax savings and cash flow benefits, thereby assisting the businesses to reinvest in automation, AI upgrades, or expansion of operations.

The Double Declining Balance (DDB) is a version of accelerated depreciation, which is expected to accommodate the higher expenses during the early years of the asset. In contrast to the straight-line method, which distributes depreciation equally, DDB front-loads expense, making it especially helpful in an industry in which assets decline in value or efficiency.

DDB is frequently applied to manufacturing plants that require expensive machines that generate their full output in a very short period, and technology companies that are using computers and servers that become obsolete very fast.

The Double Declining Balance technique is most appropriate when there is a rapid value and efficiency decline of assets or when financial reporting would be better with the recognition of depreciation of assets in the first half of the year:

The Double Declining Balance (DDB) technique presents a convenient way of accounting for the actual use of assets in financial statements. When higher depreciation is identified in earlier years, business entities are able to follow the costs with the periods within which such assets are most productive or revenue-generating, so as to present a more realistic picture of profitability.

Although DDB lowers the reported profits in the first period as a result of increased early-year depreciation, this is usually strategically beneficial. This approach is favorable to industries whose capital expenditure is enormous, such as manufacturing, transportation, energy, and technology, as it correlates accounting with the performance of the assets.

As an illustration, a factory that invests in advanced robotics or automated production lines may find that the early depreciation is offset by high levels of maintenance and operational expenses, which is a true reflection of the cash flow and profitability.

In addition to operational accuracy, DDB can improve tax strategy and financial planning. It is possible to have accelerated depreciation to enhance the amount of deductionsatn the beginning of the year that can be used to improve the cash available to be used in reinvestment, modernization, or upgrade of technology. According to studies conducted by PwC and Deloitte, capital-intensive companies with fast-tracked depreciation policies are in a better position to handle taxation expenses, finance technology adoption, and withstand variations in the market.

In the cases of businesses dealing with assets with quick depreciation, like IT infrastructure, fleet cars, or specialized equipment, the knowledge and application of DDB will ensure that financial reporting reflects the reality of an asset, which will be used to make informed investment decisions and guarantee sustainable growth.

After all, the DDB method is not an accounting tool only; it is actually a strategic way of aligning the cost of assets, efficiency in operations, and long-term financial planning in the industries where initial productivity and depreciation are of paramount importance